Money Confidence After 40: Your 30-Minute Guide to Financial Clarity

Mar 10, 2025

Money Confidence After 40: Your 30-Minute Guide to Financial Clarity

If you're stressed about money, constantly wondering, "How much should I be saving?" or "How much should I be spending?" and "why isn't there more left over at the end of the month?" You're not alone! As women over 40, it's time we felt confident about our money.

The Mid-Life Money Challenge: Why We're Worried About Money

According to a 2023 Fidelity Investments study, 65% of women over 40 report feeling uncertain about their financial future, despite earning more than previous generations.

What's this all about? It could be that we're juggling more priorities than ever: caring for aging parents, supporting children (sometimes adult ones), advancing careers, and trying to prepare for our own retirement. Add to that the historical challenges women face—longer lifespans, potential career gaps, and wage disparities—and it's no wonder we're worried about money.

But here's the truth: You don't need to be a financial expert to take control of your finances.

What we need is a simple method that quickly answers persistent questions like "How much should I spend?" and "Am I saving or earning enough?" Enter the 50/30/20 rule.

The Reality Check: How Most Americans Handle Money

Before we dive into your personal finances, let's look at how the average American manages money:

- The Federal Reserve reports the average American household saves only 5-7% of their income—far below the recommended 20%

- According to the Bureau of Labor Statistics, Americans typically spend 33% of their budget on housing alone

- The average household carries $7,951 in credit card debt (Federal Reserve Survey of Consumer Finances)

- Women are 80% more likely than men to face financial hardship in retirement (National Institute on Retirement Security)

- Most Americans spend between 17-25% of their income on non-essentials, often without realizing it

These statistics aren't meant to make you more stressed about money—they're meant to show that taking control of your finances now puts you ahead of the curve.

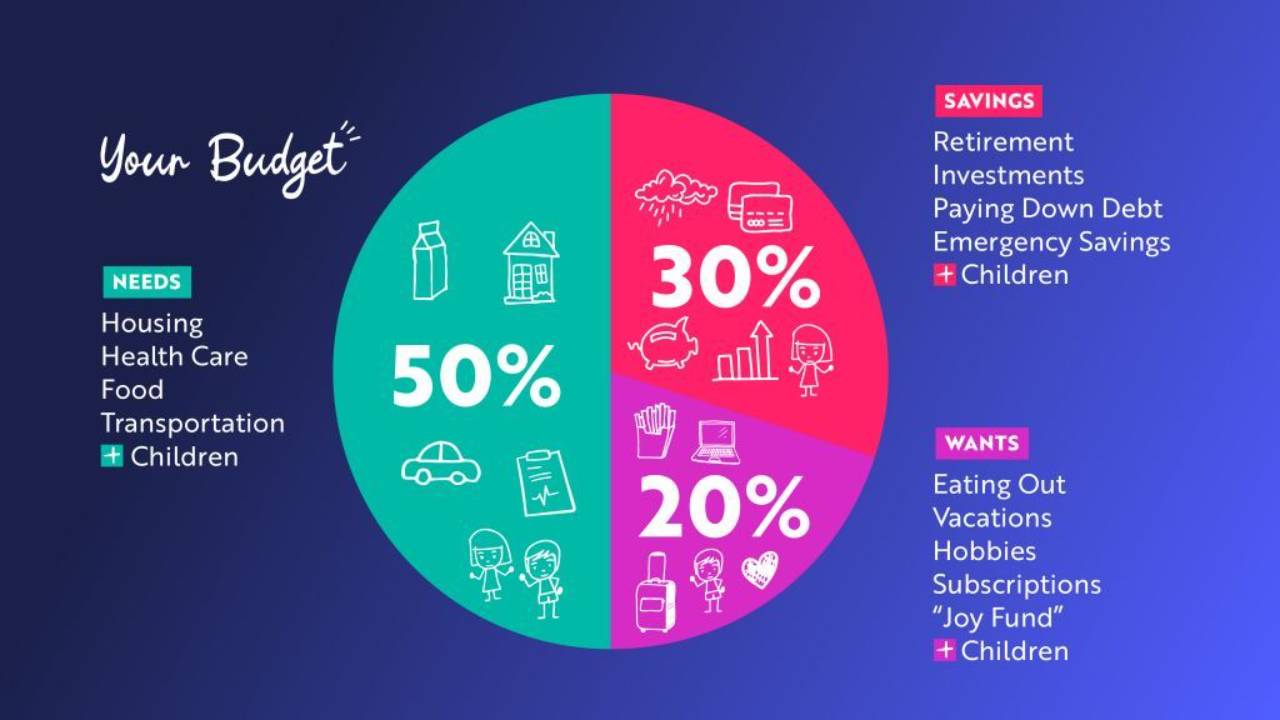

The 50/30/20 Rule: A Simple Answer to "How to Budget Your Money"

The 50/30/20 rule, popularized by Elizabeth Warren, divides your take-home pay into three clear categories:

🔹 50% Needs

These are the essentials that keep your life running smoothly:

- Housing (Mortgage or Rent)

- Utilities (Electricity, Water, Gas, Internet)

- Groceries & Household Essentials

- Transportation (Car Payment, Insurance, Gas)

- Health & Insurance

- Other Essentials: Cell phone, child care, minimum debt payment, necessary clothing, etc

🔹 30% Wants

These enhance your life but aren't necessary:

- Dining out & entertainment

- Travel & vacations

- Hobbies & leisure activities

- Non-essential shopping (designer clothes, beauty treatments, tech gadgets)

- Subscriptions & memberships

Pro tip: Some wants, like travel, may function as a savings category since you likely set money aside over time rather than spending it monthly.

🔹 20% Savings & Debt Repayment

Your future-focused financial priorities:

- Emergency fund savings (3-6 months of expenses)

- Retirement investments (401(k), IRA, brokerage accounts)

- Additional debt payments beyond minimums

Why This Works: This simple formula answers the question "How much should I spend?" with clear percentages. Most people don't realize how much they're overspending in one area, leaving little for savings or enjoyment. This rule brings awareness and balance to your finances without requiring complicated spreadsheets or constant tracking.

A Real-World Example: How Much Should I Be Saving?

Let's look at a concrete example of how the 50/30/20 rule works in practice.

Jane earns $125,000 per year with a monthly take-home pay of approximately $7,800 after taxes. Here's how her budget breaks down:

Needs (50%) → $3,900/month

🏡 Mortgage (based on a $400K home) → $2,300

🔌 Utilities → $250

🥑 Groceries & Household Essentials → $800

🚗 Car Payment, Insurance, Gas → $750

🩺 Health Insurance & Other Essentials → $400

Total: $4,500 (58% of take-home pay — slightly above target)

Wants (30%) → $2,340/month

🍽️ Dining Out & Entertainment → $350

✈️ Travel & Vacation Savings → $600

🎭 Hobbies & Leisure → $400

🛍️ Non-Essential Shopping → $500

📺 Subscriptions & Miscellaneous → $490

Total: $2,340 (30% of take-home pay — right on target)

Savings & Debt Repayment (20%) → $1,560/month

💰 Emergency Fund Savings → $500

📈 Retirement Savings → $800

💳 Additional Debt Payments → $260

Total: $1,560 (20% of take-home pay — right on target)

Notice that Jane's "Needs" category is slightly higher than the recommended 50%. This is common, especially in areas with high housing costs. The key is awareness—Jane knows this and can make informed decisions about whether to adjust.

"How Much Should I Have Saved By 40?" — Adapting to Your Income Level

The question "How much should I have saved by 40?" doesn't have a one-size-fits-all answer. Financial experts typically recommend having 3-4 times your annual salary saved for retirement by age 40, plus an emergency fund of 3-6 months of expenses.

But don't get discouraged! Regardless of where you're starting from, the 50/30/20 rule can help you move forward. It works at any income level—simply multiply your monthly take-home pay by these percentages:

- Your monthly take-home pay × 0.5 = Your needs budget

- Your monthly take-home pay × 0.3 = Your wants budget

- Your monthly take-home pay × 0.2 = Your savings/debt budget

Example:

- $5,000 monthly take-home pay:

- Needs: $5,000 × 0.5 = $2,500

- Wants: $5,000 × 0.3 = $1,500

- Savings: $5,000 × 0.2 = $1,000

Your 30-Minute Money Mapping Exercise: No More Being Stressed About Money

Now it's your turn. Set aside 30 minutes and follow these steps to reduce financial stress:

Phase 1: Gather Your Info (5-10 minutes)

- Pull up your last 3 months of bank & credit card statements

- Have a notepad or spreadsheet ready

Phase 2: Categorize & Calculate (15-20 minutes)

- Write down your monthly take-home pay

- Go through your expenses and sort them into "Needs," "Wants," and "Savings/Debt Repayment"

- Total each category for each month, then find your 3-month average

Phase 3: Compare & Plan (5-10 minutes)

- Calculate your ideal 50/30/20 breakdown using your actual income

- Compare your actual spending to the ideal percentages

- Identify 1-2 categories where adjustments would have the biggest impact

- Write down one specific action you can take this week

Remember: This exercise might take longer the first time, but the clarity you gain is worth it. Many people report that after completing this exercise, they're much less worried about money than they have been in years. Even if they see where they've been out of line, knowledge is POWER! Burying your head in the sand, doesn't make the problem go away. We all know it just makes the problem BIGGER when it's time to face it.

The Rule Is a Guide, Not a Strict Law

Maybe you live in San Francisco or New York, where housing costs can easily exceed 50% of your income. Perhaps you're in a season where the kids expenses are higher or you're investing in something, like education, for yourself and you're above the 30%. That's okay!

The 50/30/20 rule is a starting point—a way to gain awareness and make intentional choices about how to budget your money. The goal isn't perfect adherence to arbitrary percentages; it's creating a financial life that works for YOU.

What matters is having clarity about where your money goes and making conscious decisions that align with your values and goals.

Your Next Steps to Money Confidence

If you ready to take your financial clarity to the next level, let's talk!

Option 1: Free Discovery Call

Still stressed about money? Wondering how much you should be saving? Book a complimentary 20-minute discovery call to discuss your situation and see if we're a good fit. I'll answer your questions and help you determine your best next steps—no obligation.

[BOOK YOUR FREE DISCOVERY CALL →] HERE

Option 2: Guided Money Mapping Session

Ready for hands-on help with how to budget your money? In this 60-minute session ($197), we'll work through your Money Map together. I'll guide you through analyzing your statements, identifying patterns, and creating a personalized plan to optimize your finances. I'll even give you an AI cheatsheet to make it that much easier for you each month!

[BOOK YOUR GUIDED MAPPING SESSION →] HERE Use code MONEYMAP for $50 off your first session

Stay Connected for More Insights

Join My "2 Minute Transformation" Newsletter

Looking for powerful insights that transform your relationship with money, career, and self? My newsletter delivers bite-sized wisdom on Enneagram-based self-discovery, Kolbe-informed career guidance, and financial empowerment—all designed specifically for women over 40.

[YES, I WANT TRANSFORMATIVE INSIGHTS] Enter your email below

Have you tried using the 50/30/20 rule before? What was your experience? Share in the comments below!

The Quick Way to Make The Right Decision Fast

Cut out the noise and stress. Use this easy 3 step method to make decisions you can trust in less time.